If anyone is dependent on you and your ability to earn an income, you should consider insuring your life.

If you have no dependants – if you are single with no children, for example - and no debts, you may not need life cover but you should still consider disability cover.

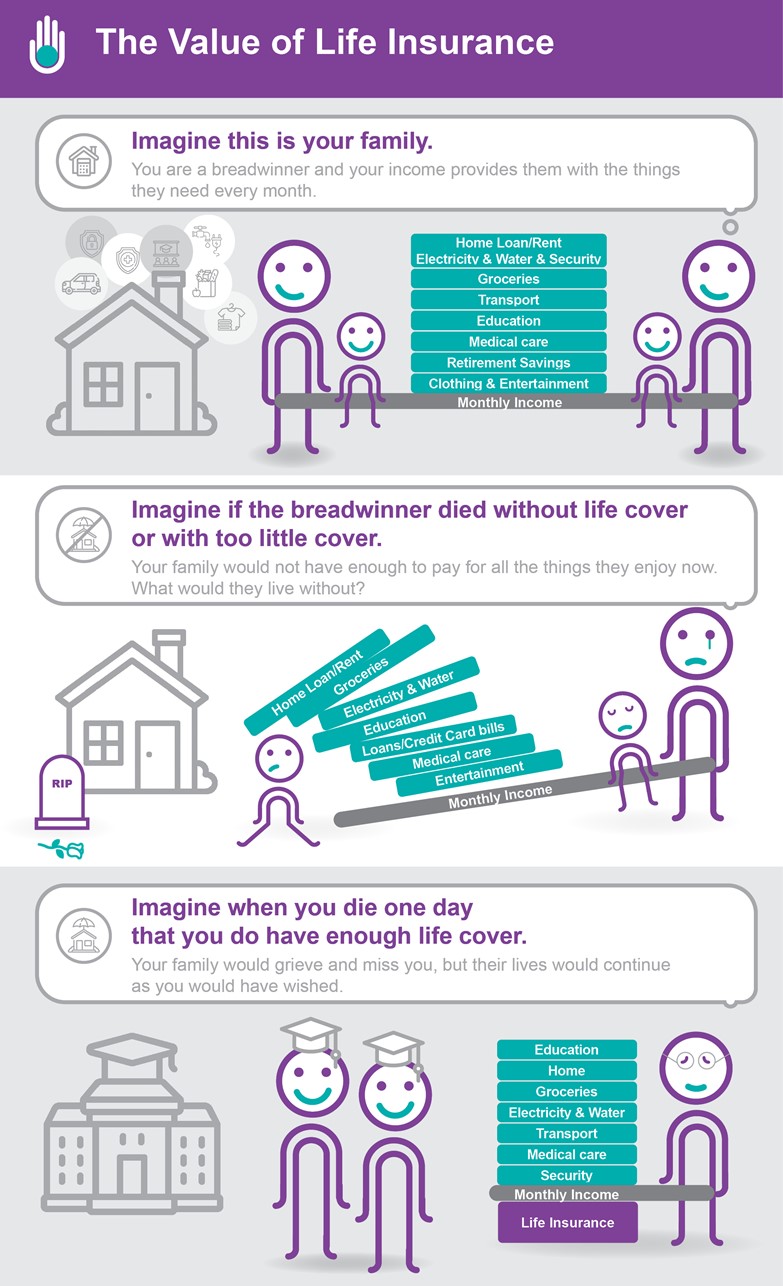

If you have a spouse, life partner, children or any other family member dependant on you for ongoing financial support, you should consider taking out life cover to ensure they have enough to sustain them should you die before retirement, or before you have saved enough to support them.

This is because the benefit paid out in the event of your early death can:

Provide your spouse or family with an income;

Pay off your debts;

Secure your home and other assets such as your car;

Ensure your savings goals such as tertiary education for your children are achieved; and

Pay your funeral costs.

If you own a business, you may also want to consider taking out life cover on a partner’s life so you can buy his or her share should he or she die while you are still operating the business.

Conversely, he or she can insure your life so he or she can buy your share should you die, ensuring that your heirs receive a fair price for the business.