Search

Search Results

How am I protected when I invest in a collective investment scheme?

Key takeaways

- Collective investment schemes are regulated through the Collective Investment Schemes Control Act and supervised by the Financial Sector Conduct Authority.

- The unit trust management company setting up a collective investment scheme must be registered by the FSCA and must meet certain operational requirements.

- The fund manager or asset manager must be licensed by the FSCA as a discretionary financial services provider.

- Each fund under the scheme has an investment mandate stating how and where it will invest and an independent trustee or custodian monitors compliance with this and the law.

- A trustee or custodian keeps each fund’s shares, bonds, cash and other investments legally secure.

- Funds are subject to some investment limits which offer you some protection but this does not guarantee your - investment which can go up or down with the markets to which it is exposed.

When you invest in a collective investment scheme, you can take comfort in the fact that it must be registered in terms of and comply with the provisions of the Collective Investment Schemes Control Act (Cisca).

The financial services regulator, the Financial Sector Conduct Authority (FSCA), regulates and supervises collective investment schemes.

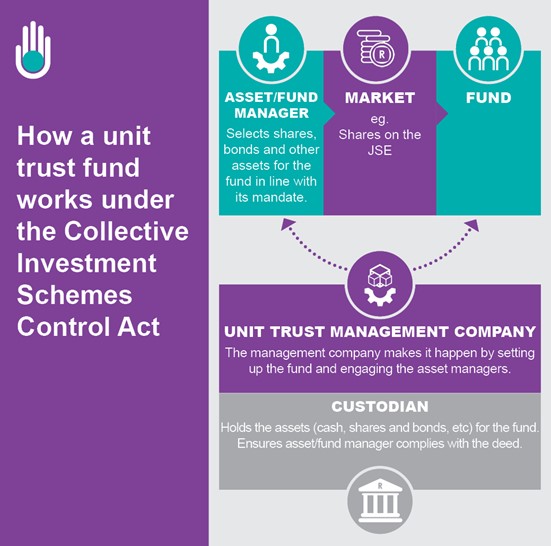

In order to set up a collective investment scheme, a financial services company must be registered by the FSCA as a management company. A company has to have a certain amount of capital to maintain its registration.

You can check if a company is registered on the FSCA’s website here.

Deed sets up scheme

The company sets up a scheme by way of a deed – a written document setting out the rules for the  administration of the scheme, establishing, in the case of a unit trust or ETF, the fund that will collect investors’ money and invest it, and your participation in it. The supplemental deed records the mandate of the fund – how it will invest.

administration of the scheme, establishing, in the case of a unit trust or ETF, the fund that will collect investors’ money and invest it, and your participation in it. The supplemental deed records the mandate of the fund – how it will invest.

The company then appoints a professional fund manager or asset manager to select the investments in line with the mandate. In many cases, the unit trust management company is in the same broader group as the asset manager.

The company then appoints a professional fund manager or asset manager to select the investments in line with the mandate. In many cases, the unit trust management company is in the same broader group as the asset manager.

The deed also sets out who the unit trust management company has appointed as custodian or trustee for the scheme – typically a bank.

The custodian must be independent of the unit trust management company, and its holding company, and the asset manager or fund manager. It must be registered with the FSCA and must also have a certain amount of capital.

The custodian or trustee holds the cash and securities in which the fund invests, and any interest or income the fund earns, in safe custody on behalf of the fund. This protects you in the event of the unit trust management company getting into financial difficulty – your investment should always be safely held by the custodian.

The trustee will also monitor that the fund manager selects investments in compliance with Cisca and the fund mandate.

Licenced

The asset manager or fund manager needs to hold what is known as a category II licence under the Financial  Advisory and Intermediary Services (FAIS) Act to provide discretionary investment management services – that is to pick investments on behalf of investors. In order to obtain this licence, the fund manager must meet certain operational and fit and proper requirements. These requirements include a level of competency.

Advisory and Intermediary Services (FAIS) Act to provide discretionary investment management services – that is to pick investments on behalf of investors. In order to obtain this licence, the fund manager must meet certain operational and fit and proper requirements. These requirements include a level of competency.

You can check if your fund or asset manager has a FAIS licence on the FSCA’s website here.

A unit trust management company and the collective investment scheme with the funds must be audited.

Assets held by funds must be valued in accordance with regulatory requirements.

The exposure to certain asset classes and how much a fund can invest in a single security is also subject to regulation. Among other things, this ensures your investment is well diversified. Read more: Are there any restrictions on unit trust funds?

While this legal protection can give you peace of mind that your money is well managed and protected from the manager’s business risk, it does not mean your investment is guaranteed to do well.

The performance of your investment in a collective investment schemes in securities will depend on the markets it is exposed to, the risks your manager takes and the securities it chooses or tracks.

Read more: How can I analyse the performance of my unit trust fund?